Materiality Mapping for ESG Assessments: Guide for Student Managed Investment Funds (SMIFs)

MSMF ESG Department (Portfolio)

First Draft: March 31, 2023

Final Revision: June 31, 2024

Materiality Map

https://public.tableau.com/app/profile/sarah.singh/viz/MaterialityMaps-ESG/Dashboard1

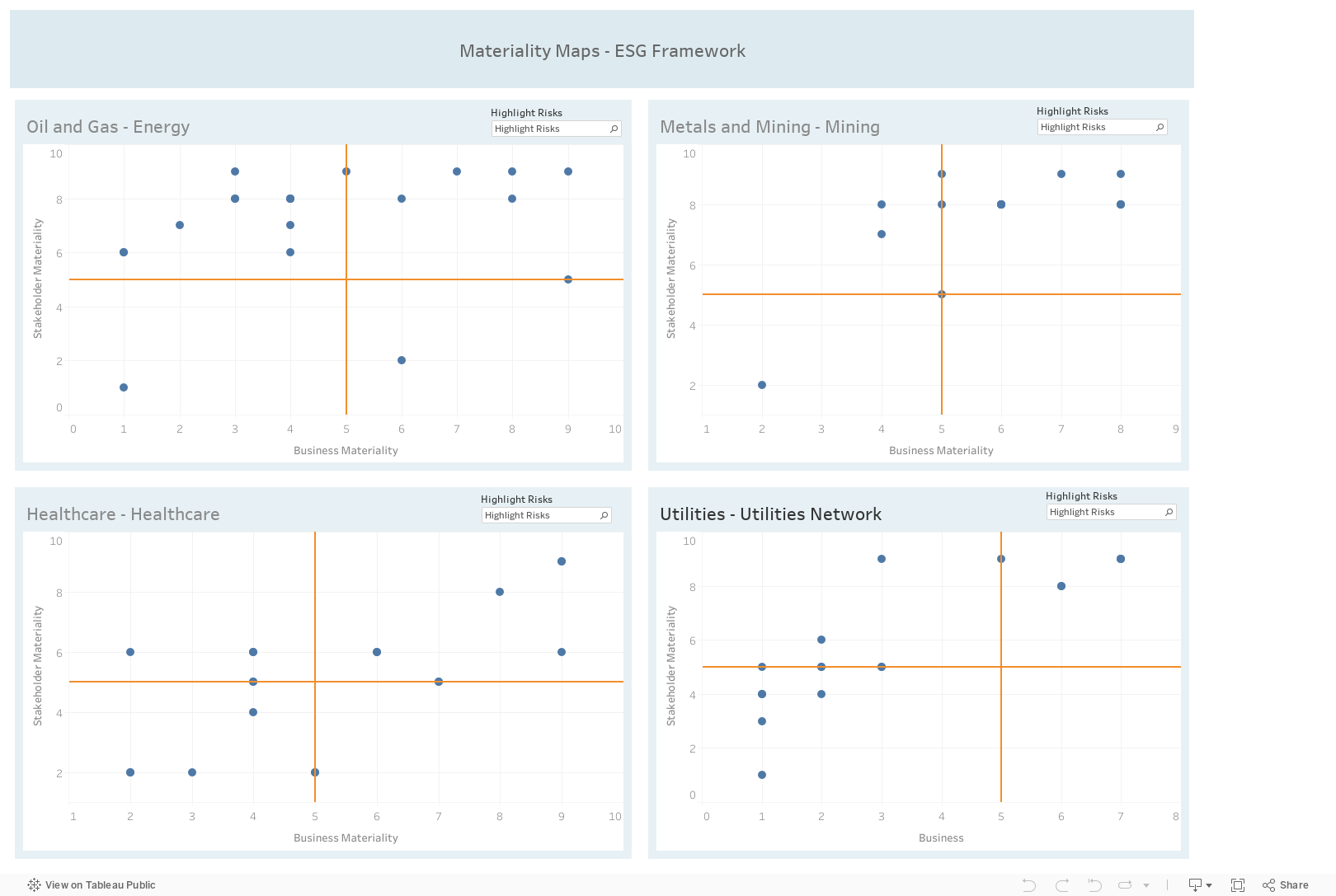

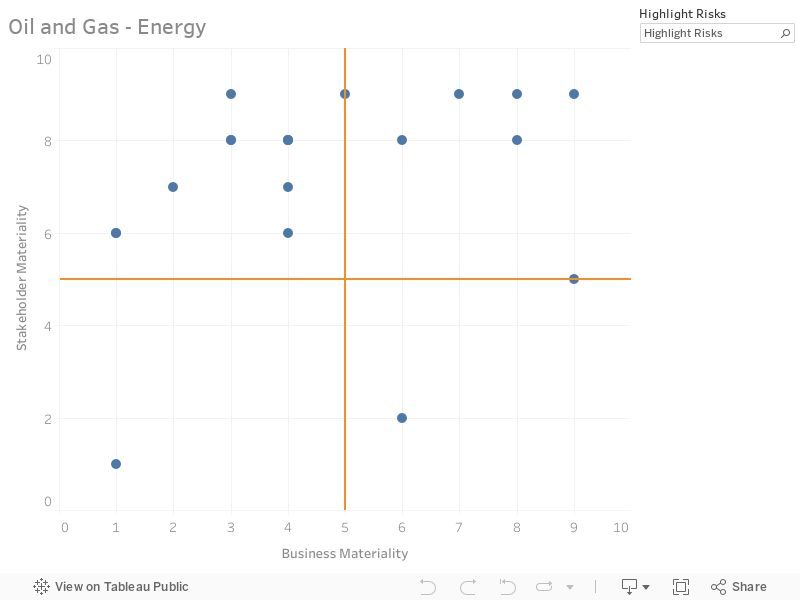

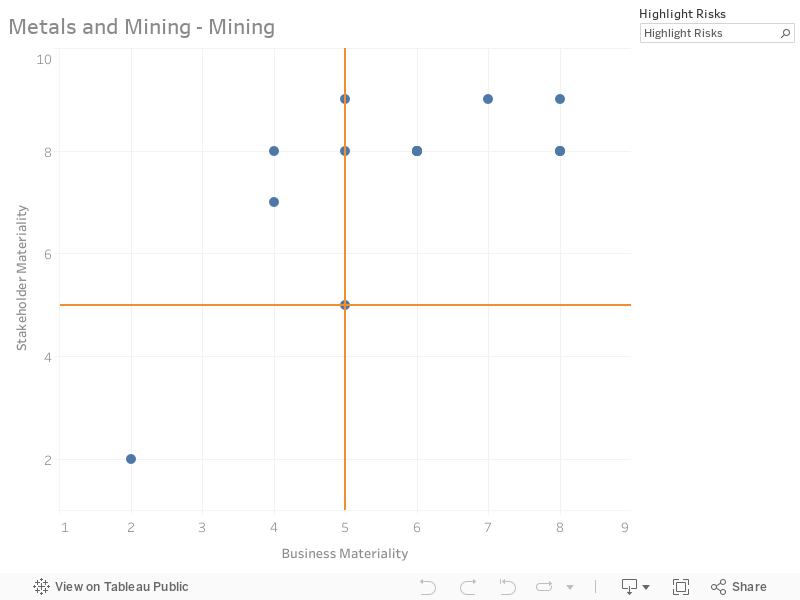

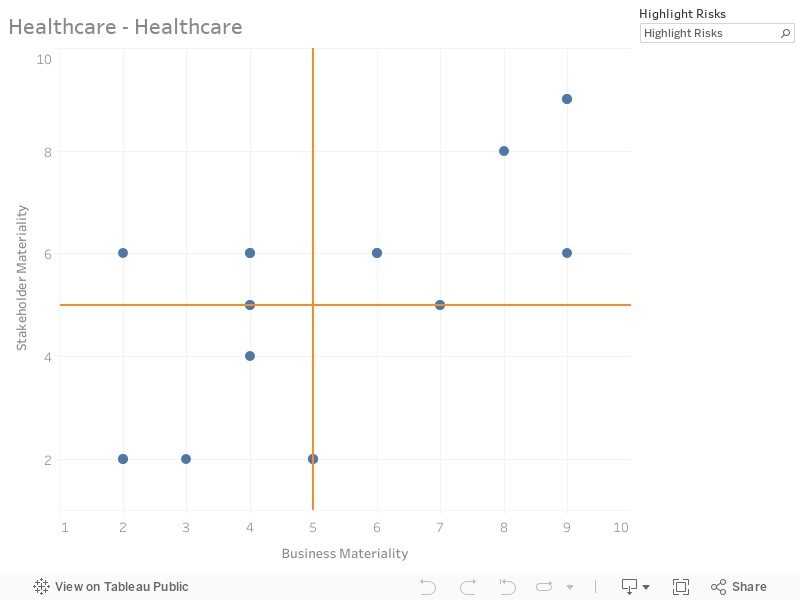

Figure 1. shows the Materiality Map with credit score and the stakeholder score on the y and x axis respectively. The scale on the legend varies from 1 to 9 for both axes. A combination of credit and stakeholder score of more than 4 has been designated as a high risk.

There are four maps dedicated to industries Oil and gas (Energy Sector), Utilities Network Industry (Utilities Sector), Healthcare Industry (Healthcare Sector), and Metals & Mining Industry (Mining Sector).

Terms and Definitions

Organisation - Monash Student Managed Fund (MSMF)

SMIF - Student Managed Investment Funds

Company - a public company subjected to valuation

Business/ Credit materiality - potential and actual impact on parameters such as revenue, expenses, cash flow, or cost of capital.

Stakeholder materiality - considers the level of impact and dependencies on the environment, society, and economy.

SASB® – Sustainability Accounting Standards Board (SASB),

ESG factors - pertains to factors that can affect a company’s short term value and are relevant in assessing a company’s long-term value. These include issues and topics in 5 major groups including: Environment (E), Social Capital (S), Human Capital, Business Model and Innovation, and Governance and Leadership (G).

Climate transition risk - includes shifts in climate and environmental policy, associated technology, and changing consumer preferences.

Physical risk - tangible and quantifiable impacts that can affect company assets & surrounding infrastructure. An example of which is the effect of climate change to weather conditions in a manufacturing location which can influence supply and demand as resource needs change amidst these conditions.

Executive Summary

The materiality maps serve as a crucial tool in aligning investment decisions and valuations with Environmental, Social, and Governance (ESG) risks. Materiality maps help organisations such as MSMF to prioritise the ESG issues that are most pertinent to their business model and industry, offering a visual and analytical guide to where their focus should lie. By leveraging materiality maps, investors and decision-makers can gain deeper insights into a company's current ESG maturity which includes an evaluation of how well the company is addressing key ESG risks and opportunities, and how these efforts align with broader industry standards and stakeholder expectations. Furthermore, these maps provide a forward-looking perspective, enabling SMIFs to anticipate future ESG trends and challenges that may affect the company’s valuation and long-term strategy. Ultimately, the use of materiality maps enhances the ability of SMIFs to integrate ESG considerations into their strategic planning, fostering a more sustainable and value-driven approach to growth. This not only supports better risk management and compliance but also contributes to creating long-term value for both the company and its stakeholders. By systematically identifying and assessing the issues that hold significance for a company's stakeholders—be they investors, customers, employees, or regulators—these maps provide a comprehensive framework for understanding how these factors impact the long-term value and sustainability of a business. In an increasingly complex and dynamic market, the relevance of ESG factors has grown, influencing not just corporate reputations but also financial performance and resilience.

Objectives

To simplify valuations of Investment teams to ESG considerations for SMIFs

To enrich the understanding of ESG issues for SMIFs

To create a open source framework that is replicable by SMIFs or any organisation without propritarydataset constraints

To allow flexibility and efficiency in assessing ESG issues whether circumstances arise from internal or external events

To establish a baseline with the organisation’s current perspective on assessing material risks on company valuations

Scope and Limitations

The current project, as it stands, serves as an initial framework for evaluating ESG (Environmental, Social, and Governance) risks across various industries and sectors. However, it is important to recognise that the current scope is limited and may not comprehensively represent all industries, sectors, and sub-sectors. This limitation underscores the need for the project's continuation and expansion when different cohorts or industry groups require assessment. The issues identified and listed for each cohort in this project are those deemed relevant to at least 50% of the companies within their respective groups. This threshold ensures a broad level of applicability, but it also implies that certain issues might be relevant to a smaller subset of companies or even to individual companies. As such, while the project's findings provide a useful baseline for valuations conducted by the Investment teams, the ESG team should remain vigilant to the possibility that some issues may be more specific and pertinent to particular companies within a cohort.

Additionally, the assessment of risk levels within this project is intentionally designed to be flexible. This flexibility is crucial because both internal factors (such as changes in company strategy, leadership, or operational processes) and external events (such as regulatory changes, market shifts, or environmental incidents) can influence an organization's perception and evaluation of risk. As a result, the project's risk assessments should be considered dynamic, with the understanding that they may need to be revisited and adjusted over time in response to evolving circumstances. While the current scope provides a valuable foundation for understanding and assessing ESG risks, its limitations highlight the importance of ongoing assessment and adaptation. The project's continuation and expansion towards other SASB Sustainable Industry Classification System® (SICS®) sectors will be essential to ensure that it remains relevant and comprehensive across a broader range of industries and sectors, and that it can address both common and unique issues that may arise within different cohorts of companies.

Methodology

This research employs a comprehensive approach to identifying and assessing material issues relevant to various industry cohorts. The process begins by referencing the SASB Materiality Map® framework as a foundational tool for identifying key issues. This framework is supplemented with sector-specific disclosure topics provided by SASB’s Sustainable Industry Classification System® (SICS®). While the SASB framework serves as a valuable starting point, it has inherent limitations, particularly in its coverage of certain risk categories.

To address these gaps, physical risks and climate transition risks have been incorporated as additional material issues for applicable cohorts. This inclusion aligns with the S&P Global Ratings system, which identifies these risks as the most significant ESG (Environmental, Social, and Governance) threats to industries such as Energy and Mining. Beyond the SASB framework, other critical issues have been identified and integrated into the model when their relevance to risk assessment is evident. This broader approach ensures a more holistic evaluation of material risks.

Subsequently, a grading system was developed to quantify the severity of identified risks. This system assigns a score from 1 to 9, with 1 representing a risk that is easily absorbable and 9 indicating a very high risk that could cause extensive damage to a company, making it highly material to both the company’s stakeholders and its business operations. SMIFs must be aware that the current state of ESG assesments are still heavily reliant on qualitative scoring therefore, SMIfs must take rigorous due diligence when conducting to assess the materiality of each issue in relation to both credit risk and stakeholder concerns with the primary references being S&P Global’s materiality maps.

However, it’s important to note that the S&P materiality maps focus predominantly on environmental and social capital factors, presenting limitations in assessing materiality associated with human capital, business innovation, and governance. To mitigate these limitations, additional due diligence was undertaken, drawing on a wider range of sources and expert opinions to strengthen the assessments and provide a more robust evaluation of these factors.

Finally, the methodology was designed with flexibility and adaptability in mind. The spreadsheet used for recording risk assessments is structured to allow for easy updates and amendments as new information becomes available or as the assessment criteria evolve. To enhance usability, a dashboard was created to visualize and summarize the findings. This dashboard is intended to be an accessible tool for investment teams and other stakeholders within the Student-Managed Investment Fund (SMIF), facilitating informed decision-making and efficient risk management.

Material Issue Topic Reading Guide

Example Materiality Maps and Justifications

Oil and Gas Industry (Energy Sector)

The scope of this analysis is most applicable to companies under the Oil and Gas Industry which include both upstream exploration and production and downstream refining with material topics based on SASB Disclosure topic Oil & Gas – Exploration & Production .This model can also be used for services like drilling and oilfield.

https://public.tableau.com/views/MSMFMaterialityMaps-OilandGas/OilandGas?:language=en-GB&:sid=&:redirect=auth&:display_count=n&:origin=viz_share_link

Climate transition risk (9,9)

Governments globally have been implementing stricter regulations, not only demanding more tax to companies who don't follow ideal emissions but also providing subsidies to companies who are successful in reducing GHG emissions.[1] More and more countries are participating in this initiative. Additionally, countries like Canada, Germany, and China, and the European Union have been aggressive in implementing additional regulations, major pricing schemes and increase in prices in 2021.[2]

Both business and stakeholders should also take into consideration the potential impact on profitability and cash generation due to possible decline in demand in the future due to the existence of alternatives.[1] The possibility of stranded assets should also be taken into consideration since the risks are also high and it may end up a liability.[1] Lastly, the occurrence of company litigation has been occurring regularly affecting many aspects of companies within this industry.[4]

GHG emissions and Air quality (8,9 ; 8,8)

The number of stakeholders supporting the reduction of GHG emissions has been constantly growing shaping the policies and trends toward a net-zero goal. With government policies and trend shifting to electric or low-carbon transportation and renewable energy, stakeholder support has started shifting towards this direction as well.[1] On the business side, both stakeholders and customers demand can decline if growth of alternatives persist. Robust and strict operational implementation is a necessity in companies under this industry since issues like methane leakage have been proven to cause damages to companies similar to MDC energy’s bankruptcy in 2019.[3]

Environmental, social aspects on core assets and operations and Physical climate risk (7,9 ; 6,8)

Climate-related physical events like sudden weather changes, flooding, landslides, and hurricanes can cause operational issues and shutdowns affecting profit. It can also create damage to equipment. Certain areas are experiencing unexpected weather and have become unpredictable especially in the long run. With oil and gas activities highly dependent on field work, an assessment of the location and other physical climate risks should be considered.[1]

Accident and safety management (9,5)

Accidents can have large financial consequences including but not limited to scarcity of manpower, damage of equipment, lost output, litigation fees, and fines by the government.[4] If not for accidents, safety auditing bodies can also halt operations if risks have been evaluated as high risks and needs fixing which can result in loss of profit.[4] An assessment of accident and safety management can be done by looking for projects dedicated for safety practices and the successes of its implementation. Frequency of news regarding accidents and safety concerns can also serve as a metric.

Lifecycle impacts of products and services (5,9)

Products, services, and operations can greatly affect the surrounding communities both positively and negatively. A good relationship with the community and an understanding for compromise can heighten shared benefits. On the other hand, local opposition can delay or raise costs for companies.[1] Additionally, an assessment of relevant government policies should be considered due to the emergence of government price caps and windfall taxes. An example of which is when UK Chancellor Jeremy Hunt declared in the 2022 Autumn statement that windfall tax would be increased to 35% on profits made from extracting oil and gas, and it will run until March 2028.[5]

2. Metals and Mining Industry (Mining Sector)

The scope of this analysis is most applicable to companies under the Metals and Mining Industry which include bulk mineral mining to advanced fabricated products with material topics based on SASB Disclosure Topic Metals & Mining. This also includes any service or processes being offered by companies utilising the processes of extracting, processing, and refining ore-bearing rock to produce metals or minerals. Additionally, this analysis is also applicable to companies engaging in the production of steel, aluminium, recycled metals, and advanced alloyed materials.

Air quality (8,8)

In essence, mining disrupts ecosystems by releasing toxic elements into the air, water, or soil, and many ores are processed with hazardous substances that could be damaging if leaked. Therefore Air Quality as a metric scores an 8 based on Stakeholder Materiality and 8 on Business Materiality.

Water and wastewater management (6,8)

In terms of stakeholder and business value, pollution is highly relevant. Pollution through mining can also harm human health by contaminating soil, air or water. There have been high remediation costs and repetitional damage due to incidents like Samarco (2015) and Brumadinho (2019) as they have detrimental effects on operations and credit worthiness. Waste and pollution (air, land and water) management is embedded within the operating plans for any assets in the metals and mining industry. However, this is with varying degrees of quality management, scrutiny, and risk. This is where an asset's profitability and risk exposure vary depending on its cost requirements.

Climate transition risks (7,9)

The metals and mining sector faces significant environmental issues material for both stakeholders and credit, with primary exposures to the climate transition. The mining of minerals and processing of metals are both energy intensive, particularly primary metals versus recycled metals. Moreover, the energy intensity of mining is increasing in many cases as ore grades decline and generally require more processing. The sector supports the energy transition, as it could benefit both stakeholders and credit for companies producing a few essential metals like copper, lithium, cobalt, or nickel.

GHG emissions (8,9)

There is a high direct and indirect carbon intensity in the sector, it emits pollutants, and it sometimes causes pollution incidents that harm people and natural ecosystems. Coal combustion produces significant greenhouse gas emissions (GHG). As coal is a cheaper and more abundant fuel source globally, phasing out coal affects stakeholders by potentially raising electricity prices. It is also a significant economic contributor in many localities. Energy transitions result in weaker demand and greater credit risk for coal companies, and they are spilling over into the most energy-intensive segments of the wider industry. For example, steel is produced with coal-fired blast furnaces and Aluminium, by comparison, has attractive (lightweight and recyclability) properties but its production uses carbon anodes, which also emit significant GHGs. While the energy transition presents significant challenges for both credit and stakeholders, it relies on the use of metals like copper, lithium, cobalt, and nickel, which are essential for electrification and battery deployment.

Workforce health and safety (8,8)

Workforce health and safety factor is highly material for stakeholders and material for credit, given heavy ongoing investments in health, safety, and education to bolster safe operations. According to the International Labor Organization, the mining industry is one of the most hazardous in the world. Extractive and transformation processes expose individuals to heavy machinery and high temperatures (among other hazards), necessitating ongoing investment in safety and training, often with stringent regulatory scrutiny. Low-probability events like mine collapses or fugitive emissions can harm employees and communities, while disrupting production and prompting costly remediation, which could affect credit by increasing operational costs and potentially leading to legal liabilities. Additionally, such events can tarnish a company's reputation, impacting investor confidence and stakeholder trust. Companies in the mining sector must prioritize health and safety as a critical component of their risk management strategy. By doing so, they not only safeguard their workforce and surrounding communities but also ensure operational continuity and maintain favorable credit conditions. Robust health and safety measures can also mitigate the risk of regulatory penalties and enhance long-term sustainability, making them essential for the overall financial and operational health of mining companies.

Human Rights and Community relations (5,9)

Safety incidents may have an extensive impact on stakeholders as they can result in operational disruptions or human casualties, potentially causing friction in communities or regulatory penalties. In addition, the sector’s impact on communities is typically more pronounced for stakeholders than for the business (credit) side, considering the investments associated with large, disruptive assets. Mine plans incorporate sizable investments that can affect local living conditions, such as infrastructure. Despite these modern advancements, dissent is common, especially in conflict zones and in remote areas, where mining concessions encroach upon natural areas. While metals fabricators are less acutely exposed to this, they often have a significant footprint and presence in the communities where they operate, necessitating long standing relations with employees, pensioners, and their families. In addition, as deposits are constantly depleted, communities explore vast, new areas, causing friction, particularly with indigenous communities.

Working conditions And Employment practices

Working conditions and employment practices affect a high number of stakeholders, especially in remote regions where employees and their families are economically dependent on a small number of employers. Some employees or contractors may not be protected by robust mining or labor codes or lack awareness of their rights, leading to the possibility of exploitation with limited recourse. Other employment issues could include fair wages with appropriate benefits for often dangerous or difficult work, and ongoing training, especially on safety. Working conditions and employment practices in mining can vary by operation, but still have a relatively high credit materiality. A shortage of skilled labor often results in higher costs and higher management intensity. Despite their importance, human rights are a small and unregulated subsector of the global mining industry.

3. Healthcare Sector

The healthcare sector covers a broad range of companies, however, many issues and aspects of ESG materiality coincides with each other this section covers material topics based on all SASB Disclosure topic listed under Healthcare. With the healthcare sector is composed of these industries: Biotechnology, Pharmaceuticals, Medical Equipment and Supplies, Health Care Delivery, Healthcare Distribution, and Managed Care. [6]

Product quality and safety (9,9)

Ensuring products are manufactured within appropriate quality assurance standards has been at the forefront of the Healthcare industry. Problems with products and services can result in unwanted litigation and the temporary discontinuation of selling a product or service. There were also situations which made authorities pull-out the distribution of certain products from the market due to issues with product quality and safety.[7] This issue is very material for both business and stakeholders since discontinuation of distribution of certain products means absence of return in capital allocated for manufacturing operations, research and development, and use of resources. It can also affect the reputation of both companies and stakeholders since most pharmaceutical companies produce medication under a brand name, safety issues concerning one of its products can affect the trust of the people towards the whole brand.

Customer welfare and Access and affordability (9,9 ; 8,8)

In 2022, Ritalin, a leading ADHD treatment, fell victim to the supply chain crunch in Australia. Ritalin is supplied by Novartis Pharmaceuticals. In a statement, Novartis indicated that the problem came from the increasing prices of goods affecting the prices of raw materials necessary to make the medication.[8] However, this statement was only released later on. This created a lot of frustrations among the users due to Novartis not making an earlier announcement making users unsure of whether they need to move to another medication and tolerate the adjustment period of the body to the new medication or wait for supplies to be available and risk having withdrawal symptoms.[9] Due to this late statement and late response of the company, many users have moved to use a different medication called vyvanse causing loss in demand and brand loyalty. This is a normal occurrence wherein a competitor would react on this opportunity by intensifying the recalling firm’s damages.[7]

Data security and privacy (9, 6)

Medical data is mostly composed of very private information and is considered to be highly confidential. Many laws and regulations pertain to data privacy act and the associated penalties for its breach, misuse, and mismanagement. Due to this status of medical records and information, data security and privacy has been deemed to be a high risk that is not easily absorbable if a situation under this topic arises. An example of which is the data breach issue in 2019 of the American Medical Collection Agency (AMCA). The hacking lasted from August of 2018 till March of 2019 and it has affected at least 20 million US citizens. It followed multiple class-actions resulting in AMCA filing for bankruptcy. [11]

Materials sourcing and supply chain management (7,5 ; 6,6)

Figure 5. Novartis ESG Impact Clusters

Looking at Novartis materiality map in Figure 5. It doesn’t include materials sourcing as one of its key issues. [10] Compared to the other companies in the same industry which include materials sourcing, Novartis has faced problems with its supply chain due to problems with raw materials needed for production. Supplies of medication for heart problems, ADHD, and many more have been not available for weeks to the public creating profit losses, loss of trust, and damage to brand reputation.[9] This also shows that an assessment of a company’s self-evaluation for materiality should also be critically assessed in contrast to other companies within the same cohort or the overarching industry or sector.

Business ethics and transparency (7,5)

A responsibly managed company is important to the long-term value of a business. This is why it appears to be more relevant to the business compared to the stakeholders. A company with good business ethics and transparency incorporates rule-based decision making, clear checks and balances, and goals that are in line with the social, regulatory, and market environment. This has been deemed very important since the healthcare sector directly impacts life and health in general. [12]

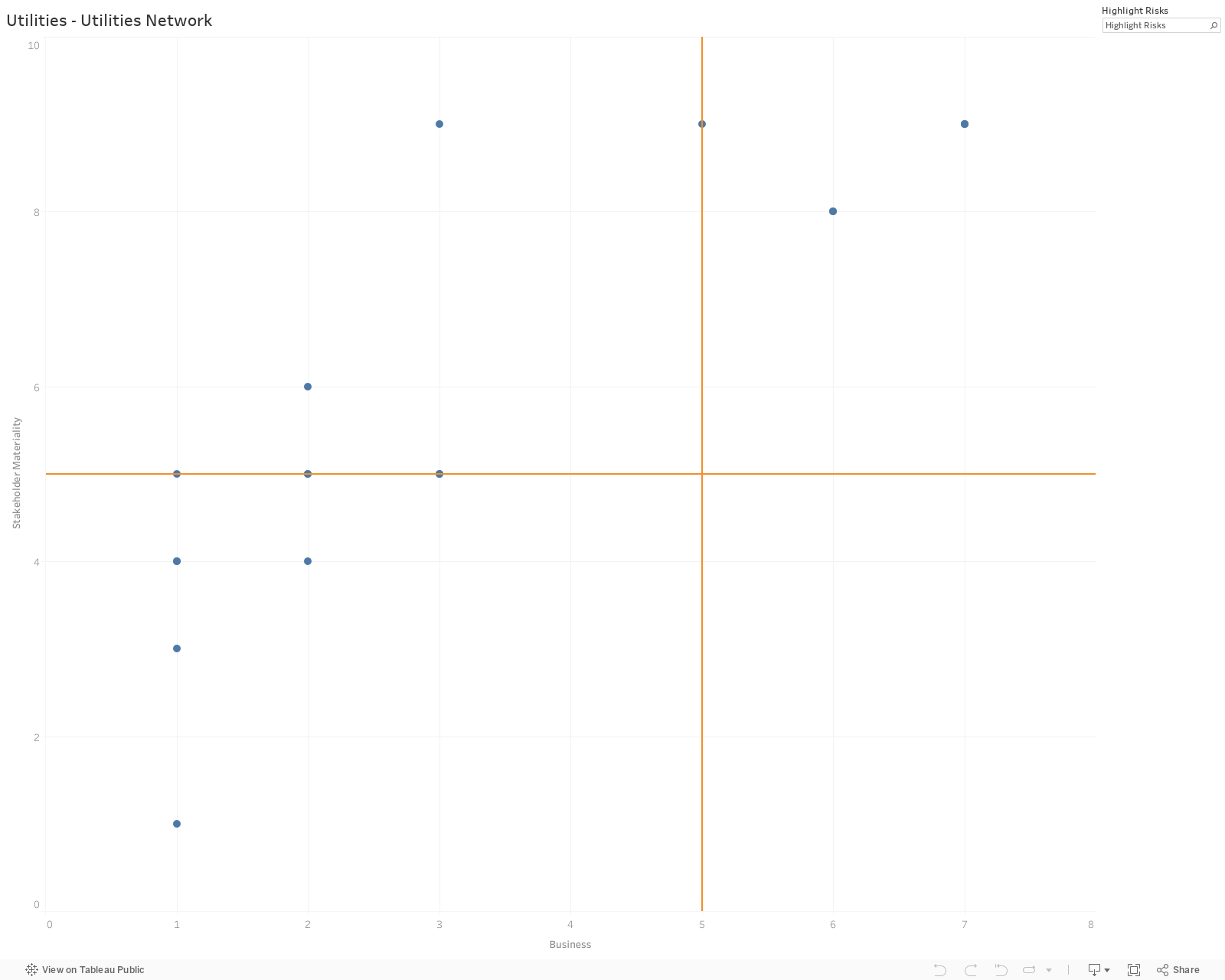

4. Utilities Sector

The Utilities network sector includes SASB Disclosure Topics from electric grids, gas utilities and water utilities companies. It also includes the transmission and distribution of these utility services. [13]

Physical risks (8,8)

Companies under this sector services large coverages. This means that they are highly susceptible to physical risks especially with the interconnectedness of networks, products and services. These conditions, especially those associated with the changing weather and weather disasters expose the sector to service disruptions. Additionally, the frequency and severity of these cases added to the unpredictability caused by climate change incurs higher costs. [14]

Climate transition risks (8,8)

This issue is very relevant to this sector especially to the electricity and gas networks because of their essential participation in the energy delivery chain and upstream generators which are considered to be a big cause of climate change. This opens these companies to risk associated with public, political, legal and regulatory pressures to accelerate initiatives addressing issues about climate. [15]

“From a credit perspective, the ongoing decarbonization of the energy sector requires a tripling of renewable power, which comes with significant grid expansion. As such, network capital budgets are near record highs, leveraging their balance sheets and pressuring credit quality. In the gas network sector, continued focus on reducing reliance on methane-emitting natural gas could diminish growth prospects, making it more difficult to effectively manage regulatory risk” - Bendersky & Grosberg 2022.

Biodiversity impacts and GHG emissions (7,9 ; 7,9)

Policies are continuously moving towards the decarbonization of economies, hence, companies within this sector should be able to respond effectively to remain competitive. [15] Possible sources of sunk costs especially to big and long-term projects should be monitored accordingly. A company’s strategic allocation of investments to non-carbon assets and transition enablers have been continuously growing among companies under this sector to prepare for the impact of climate transition risk expected to happen in the near future given the trend of stakeholders’ perspective. Lastly, it won’t hurt to have a brief understanding of what constitutes a licence to operate within this sector. [14]

Waste and hazardous materials management and Energy management (7,9 ; 6,8)

These networks tend to be close to community settlement which can affect the overall risk of health, safety, and well-being of community members and the surrounding habitat through fires, service disruptions, gas explosions, contaminated drinking water and untreated wastewater. These damages can be made irreversible creating high risk to stakeholders. With these networks having a model who work closely with the people, government and regulators, accidents like these can undermine public trust and affect a company’s licence to operate.[14]

Access and affordability (5,9)

Products associated with electricity, gas, and water have been deeply integrated into the daily lives of community members. That being said, considerations for this sector cannot just be limited to its interaction with global economic development, but also human health and well-being. Due to its integration to daily lives, issues within this sector can affect a household’s purchasing power and the competitive strengths of local industries making it a very relevant issue from a stakeholder perspective. [14] However, its credit materiality rating is not as high due to the participation of the government in these services allowing it to regulate volatility of prices. On that note, analysts should be made aware that too much involvement of the government comes with its own disadvantages, hence, making this issue a double-edged sword. [16]

4. ESG Assessment Example: IT Services- WiseTech Global (ASX:WTC)

Further Recommendations

Continuously Add Sectors, Sub-Sectors, and Industries Relevant to the Portfolio: To maintain a comprehensive understanding of risk across diverse areas, it is crucial to continually update and expand the range of sectors, sub-sectors, and industries covered in the portfolio. This ongoing process ensures that emerging risks and industry-specific challenges are effectively identified and managed. By staying current with industry trends and developments, the Materiality Map can better reflect the dynamic nature of global markets, ultimately leading to more informed decision-making and ESG risk management.

Consideration of a Model Incorporating Both Risks and Opportunities: While risk assessment is vital, a model that also considers opportunities could provide a more balanced view of potential outcomes. Identifying opportunities alongside risks allows for a proactive approach, where potential gains can be maximised while mitigating threats. This double materiality model could enhance strategic planning and help in identifying areas where investments might yield significant returns, contributing to overall portfolio ESG resilience and growth.

Integration with ESG Scorecards for Assigning Issue Weights: Integrating the risk model with ESG (Environmental, Social, and Governance) scorecards can provide a more nuanced approach to assigning weights to specific issues. By aligning the risk assessment with ESG criteria, organizations can ensure that they are addressing the most material issues in a manner consistent with broader sustainability goals. This integration can also enhance transparency and accountability in how risks are managed, ultimately supporting more sustainable business practices.

Professional Consultation with Industry Experts: Engaging with industry experts through professional consultation can provide valuable insights and enhance the effectiveness of the risk management process. Experts can offer in-depth knowledge of specific sectors, helping to identify nuanced risks and opportunities that may not be immediately apparent. Their guidance can also assist in refining models and approaches, ensuring that they are aligned with industry best practices and regulatory requirements.

Transitioning to Alternative Risk Identification Models: As ESG factors become more deeply integrated into valuations, it may be beneficial to switch to a different model for identifying the level of risks, rather than relying solely on quadrant-based approaches. Moving to models that reflect industry sustainability norms and more sophisticated risk assessment methodologies can improve the accuracy and relevance of the analysis. This shift would ensure that the risk identification process remains aligned with evolving industry standards and best practices.

Further Improving Dashboards for Efficient Information Dissemination: Enhancing the dashboards used for reporting and disseminating information can significantly improve efficiency and accessibility. By refining the design and functionality of dashboards, organizations can ensure that critical information is presented clearly and in a user-friendly format. This improvement can facilitate quicker decision-making, better communication among stakeholders, and a more effective response to emerging risks and opportunities.

-

We are grateful for Prof. Deep Kapur and the team at Monash Centre for Financial Studies (MCFS) for their unwavering support on a student-led initiative and the delivery of our agenda in multiple of ways and acknowledge their contributions to each and all releases. We also remain deeply grateful to the Faculty of Banking and Finance at Monash Business School for continuous support in facilitation of MSMF and our agenda.

-

Disclamer

This material is a product of Monash Student Managed Fund (MSMF) and is provided to you solely for general information purposes. I understand that the information in these documents is NOT financial advice. Before making an investment decision to acquire shares, you should consider, preferably with the assistance of a financial or other professional adviser, whether an investment is appropriate in light of your own personal circumstances. If you can, you should obtain a copy of the Information Memorandum of the company that you are seeking to invest in, and consider their risks and disclosures. Subject to the Australian Consumer Law, Corporations Act, the ASIC Act, and any other relevant law, MSMF does not accept any responsibility for any loss to any person incurred as a result of reliance on the information, including any negligent errors or omissions. This information is strictly the personal opinion of an MSMF member and does not represent the views of MSMF. This information constitutes factual information that is objectively ascertainable such that the truth or accuracy of which cannot reasonably be questioned. MSMF does not intend to advertise any stock or financial product whatsoever. Past performance is not a reliable indicator of future performance. Past asset allocation and gearing levels may not be reliable indicators of future asset allocation and gearing levels. Performance data is just an estimation based on public market data and may not be a true reflection of actual fund performance

-

Footnotes

Ferguson M, Okasmaa E, Watters T. ESG Materiality Map: Oil and Gas. S&P Global Ratings. May 18, 2022. https://www.spglobal.com/_assets/documents/ratings/research/101560765.pdf

IMF/OECD. Tax Policy and CLimate Change: IMF/OECD Report for the G20 Finance Ministers and Central Bank Governors. September 2021. https://www.oecd.org/tax/tax-policy/tax-policy-and-climate-change-imf-oecd-g20-report-september-2021.pdf

Tabuchi H. Fracking Firms Fail, Rewarding Executives and Raising Climate Fears. The New York Times. July 12, 2021. https://www.nytimes.com/2020/07/12/climate/oil-fracking-bankruptcy-methane-executive-pay.html

Mignan A, Spada M, Burgherr P, et al. Dynamics of severe accidents in the oil & gas energy sector derived from the authoritative energy-related severe accident database. Plos One. 2022; 17(2). 10.1371/journal.pone.0263962

BBC News. What is the windfall tax on oil and gas companies?. February 16, 2023. https://www.bbc.com/news/business-60295177

Jabouley B, Marleau D. ESG Materiality Map Metals and Mining. S&P Global Ratings. May 18, 2022. https://www.spglobal.com/_assets/documents/ratings/research/101560762.pdf

SASB. Health Care Industry Research Briefs. 2023. https://www.sasb.org/standards/archive/health-care-industry-briefs/

Mukherjee A. The impact of product recall on advertising decisions and firm profit while envisioning crisis or being hazard myopic. European Journal of Operational Research. 2021; 288(3): 953-970.https://doi.org/10.1016/j.ejor.2020.06.021

Commonwealth of Australia. Methylphenidate hydrochloride - medicine shortage information. Department of Health and Aged Care. 2023. https://apps.tga.gov.au/shortages/Search/Details/methylphenidate%20hydrochloride

Lewin R. The latest product falling victim to supply chain issues is sparking major concerns among health practitioners. 7 News. August 5, 2022. https://7news.com.au/lifestyle/medicine/the-latest-product-falling-victim-to-supply-chain-issues-is-sparking-major-concerns-among-health-practitioners--c-7768442

Novartis. Global Materiality Assessment 2021 results report. 2021. https://www.novartis.com/sites/novartis_com/files/global-materiality-assessment-2021-report.pdf

Hill J. Debt Collector goes bankrupt after health care data hack. Bloomberg. June 18, 2019. https://www.bloomberg.com/news/articles/2019-06-17/american-medical-collection-agency-parent-files-for-bankruptcy#xj4y7vzkg

Philip Morris International. 2021 Sustainability Report. February 2022. https://www.pmi.com/resources/docs/default-source/pmi-sustainability/pmi-2021-sustainability-materiality-report.pdf

14. Bendersky C, Grosberg G. ESG Materiality Map Utilities Network. S&P Global Ratings. May 18, 2022. https://www.spglobal.com/_assets/documents/ratings/research/101560768.pdf

Fiduciary Trust International. Climate Change Risk and Opportunities in the Utilities Sector. August 1, 2022. https://www.fiduciarytrust.com/insights/article-detail/sustainable-investing/climate-change-risk-and-opportunities-in-the-utilities-sector

Murphy, C. Utilities and the Utilities Sector: pros and Cons for investors. Investopedia. August 15, 2022. https://www.investopedia.com/terms/u/utilities_sector.asp

Authors

Daniel Giam (Jun Wei)

Head of ESG and Sustainability

junwei.giam@monashmsmf.org

Zongjun Zhang (Devin)

Deputy Director- ESG

Xavier Tagubat

Sarah Singh