The Rise of Private Credit in Australia

1. ABSTRACT

Private credit has risen exponentially in size post-pandemic, this gave private credit the opportunity to emerge as a significant alternative financing source in Australia which has experienced rapid growth over the past decade. This commentary examines the drivers behind the expansion of private credit, analyses its financial benefits and associated risks, and projects its future trajectory within Australia’s financial landscape.

I will highlight the factors contributing to the rise of private credit, including regulatory changes, institutional investment shifts, and economic conditions.

The findings suggest that while private credit offers attractive returns and flexibility, it also presents challenges related to liquidity, credit risk, and regulatory oversight. The paper concludes with insights into the potential growth of the sector and its implications for investors and borrowers alike.

2. INTRODUCTION

The Australian financial landscape has witnessed a significant shift with the rapid rise of private credit as an alternative source of financing for businesses. This refers to debt provided directly to companies by non-ADIs, over the past years private credit has grown into a multi-billion-dollar global market. In Australia, this growth result is from the changes in banking regulations, investor behaviour, and economic conditions.

Private credit has become an increasingly important component of global finance, filling gaps left by traditional banking systems (ANZ, Westpac, CBA, NAB). Previous studies have highlighted the role of regulatory changes and the search for higher returns/yields as key factors in the growth of private credit markets. In Australia, the impact of the Royal Commission’s findings 2019 and the subsequent tightening of bank lending practices have been noted as significant contributors to the shift towards private credit.

3. MARKET DRIVERS AND GROWTH STATISTICS

A. Banking Regulations

Following the Royal Commission’s findings in 2019, Australian banks implemented stricter lending standards. This shift made it more challenging for businesses, especially small and mid-sized enterprises (SMEs), to secure traditional commercial loans. Private credit providers have stepped in to fill this gap. In 2022, private credit accounted for 30% of total debt financing for mid-market companies, with expectations to reach 40% by 2025.

B. Institutional Investment

Australian superannuation funds have increasingly allocated resources to private credit. By 2023, 15% of their alternative investments-approximately $45 billion were dedicated to private debt. This trend is driven by the higher yields offered by private credit compared to public debt markets (corporate bonds).

C. Inflation Hedge

Certain types of private credit, such as floating-rate loans, can serve as a hedge against inflation. Since the interest payments on floating-rate loans adjust with changes in interest rates, the income generated from these loans tends to rise during inflationary periods, protecting investors from the erosive effects of inflation.

4. FINANCIAL BENEFITS OF PRIVATE CREDIT

A. Attractive Yield

Private credit offers yields between 6% and 10%, outpacing traditional corporate bonds and sovereign debt. In 2023, the average yield on Australian private credit deals was 7.5%, compared to a 3.2% average yield on government bonds.

B. Deal Flexibility

Borrowers benefit from customized loan structures in private credit arrangements. This flexibility has made private credit instrumental in leveraged buyouts (LBOs) and other corporate finance activities. In 2023, $25 billion of private credit was directed toward Mergers and Acquisitions in Australia, particularly benefiting mid-market businesses.

C. Speed of Execution

Private credit providers operate with fewer regulatory constraints than banks, allowing for quicker deal closures. The average time to finalize a private credit deal in 2023 was 45 days, compared to 90-120 days for traditional bank loans- reasons that can be attributed to this are

Non - ADI, therefore ASIC and APRA have less regulations imposed

Flatter Organizational hierarchy (direct private funding from High-Net-Worth

Individuals) with knowledge of CAR (capital at risk) and selected exposures to

different industries

Capital made to be deployed, unlike banks which may need to account for more items

and manage balance sheets more cautiously

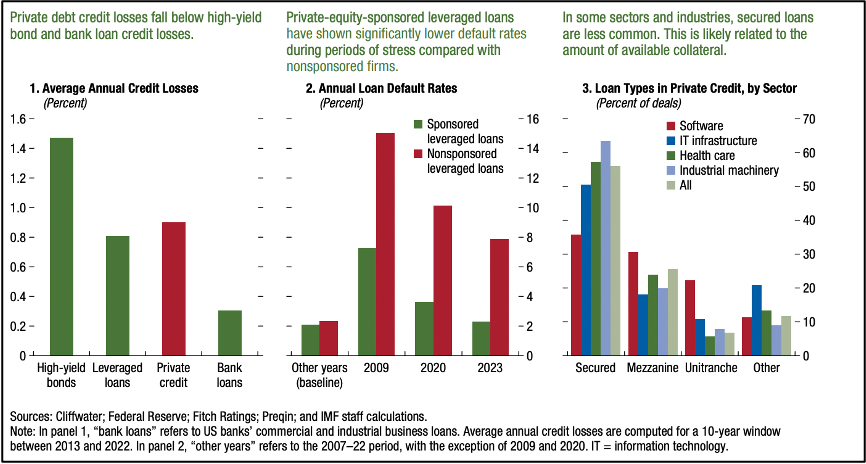

5. RISKS AND CHALLENGES OF PRIVATE CREDIT

A. Liquidity Risk

Private credit is generally illiquid, lacking the secondary market (where loans are packaged and sold) trading options which are available to publicly traded bonds. In a 2022 survey, 40% of institutional investors cited liquidity concerns as a key barrier to increasing their private credit allocations.

B. Credit Risk

Targeting mid-market businesses inherently carries higher credit risk. In 2023, the default rate for Australian private credit was 2.8%, compared to 1.2% for traditional corporate bonds. Limited transparency and regulatory oversight can amplify these risks.

C. How to mitigate these risks?

Investors may choose funds or managed accounts with explicitly longer lock-up periods, providing portfolio managers greater flexibility in managing liquidity while still seeking higher returns. Additionally, contractual lock-up terms can be negotiated to balance liquidity demands. Lenders can also negotiate stronger covenants, such as financial maintenance covenants or restrictive covenants, to provide greater control and early warning mechanisms in the event of deteriorating borrower performance. Structuring loans with seniority in the capital structure, along with collateral security, can also help mitigate potential losses in case of default.

6. FUTURE OUTLOOK AND MARKET PROJECTIONS

A. Supply - Side Growth

Institutional investors are expected to further increase their allocations to private credit. Projections indicate that by 2027, private credit AUM in Australia will reach $200 billion, representing a CAGR of 10%. The entry of cross-border private equity firms is also injecting new capital into the domestic market through foreign partnerships and FDIs

B. Demand - Side Growth

Businesses, especially SMEs and mid-market companies, will continue to seek private credit as banks maintain tighter lending standards, tightening serviceability on the loans and stricter lending policies- Private credit financed 40% of total M&A activity in the mid-market sector in 2023, with expectations to grow to 50% by 2025.

C. ESG and Impact Investing

Environmental, Social, and Governance (ESG) considerations are increasingly influencing private credit deals. In 2023, 20% of private credit transactions in Australia included an ESG component, focusing on sustainable projects in renewable energy and affordable housing. This may continue to increase given the shorter adaptability and pivot by the major banks to offering “green” loans

7. CONCLUSION

The growth of private credit in Australia reflects the result of regulatory changes, investor strategies, market demands & macro-economic forces. While offering higher yields and greater flexibility, the sector also presents heightened risks that require careful management. The potential introduction of increased regulatory oversight by APRA suggests a recognition of these risks and a move towards ensuring the sector’s stability.

Private credit has become a significant force in Australia’s financial ecosystem, providing essential financing options for businesses and attractive returns for investors. However, the sector’s rapid growth requires a balanced approach to risk management and regulatory oversight. As private credit continues to expand, it will undoubtably play a crucial role in shaping Australia’s financial future, particularly in supporting SMEs, facilitating M&A activity, and promoting ESG initiatives.

-

A special thanks to my tutor Minu Scaria & Chief Examiner for BTF3601 (Banking Law), whose guidance and encouragement throughout this unit has provided me great motivating on writing this commentary.

I am also grateful to Hassan Naqvi (Course Director, Master of Banking and Finance, International Study Program Coordinator) for his review of this commentary and feedback provided.

We are grateful for Prof. Deep Kapur and the team at Monash Centre for Financial Studies (MCFS) for their unwavering support on a student-led initiative and the delivery of our agenda in multiple of ways and acknowledge their contributions to each and all releases. We also remain deeply grateful to the Faculty of Banking and Finance at Monash Business School for continuous support in facilitation of MSMF and our agenda. -

Disclamer

This material is a product of Monash Student Managed Fund (MSMF) and is provided to you solely for general information purposes. I understand that the information in these documents is NOT financial advice. Before making an investment decision to acquire shares, you should consider, preferably with the assistance of a financial or other professional adviser, whether an investment is appropriate in light of your own personal circumstances. If you can, you should obtain a copy of the Information Memorandum of the company that you are seeking to invest in, and consider their risks and disclosures. Subject to the Australian Consumer Law, Corporations Act, the ASIC Act, and any other relevant law, MSMF does not accept any responsibility for any loss to any person incurred as a result of reliance on the information, including any negligent errors or omissions. This information is strictly the personal opinion of an MSMF member and does not represent the views of MSMF. This information constitutes factual information that is objectively ascertainable such that the truth or accuracy of which cannot reasonably be questioned. MSMF does not intend to advertise any stock or financial product whatsoever. Past performance is not a reliable indicator of future performance. Past asset allocation and gearing levels may not be reliable indicators of future asset allocation and gearing levels. Performance data is just an estimation based on public market data and may not be a true reflection of actual fund performance

-

Andre Chinnery, W. M. (October 17, 2024). Growth in Global Private Credit. Sydney: RBA.

APRA. (2022). Annual Report 2021-22. Sydney: APRA.

Fuad Faridi, J. S.-H. (September 24, 2024). The next era of private credit. Mckinsey & Company- Private Capital, 8.

McMahon, S. (2023). AustralianSuper increases Churchill Asset Management partnership to US$1.5 billion. Press Release (p. 3). Sydney: Australian Super.

Richard Rosenthal, J. H. (2024). How can banks adapt to the growth of private credit? London: Deloitte Center for Financial Services.

Shapiro, A. W. (July 1, 2024). ‘Marking their own homework’: Inside Australia’s $200b unregulated private credit boom. Financial Review.

Author